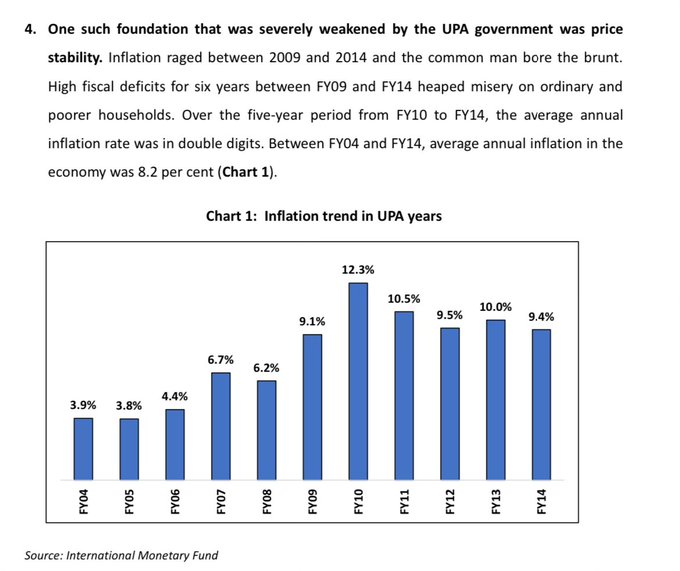

What UPA inherited from Vajpayee ji in 2004 is summed up in this way: “ In 2004, when the UPA government began its term, the economy was growing at 8 per cent (with industry and services sector growth above 7 per cent each and a resuscitating agriculture sector growth above 9 per cent in FY04) amidst a benign world economic environment.” From a healthy economy in 2004 to a stagnant economy in 2014.. Ironically, the UPA leadership, which seldom fails to take credit for the 1991 reforms, abandoned them after coming to power in 2004. Even as the country was standing at the cusp of emerging as a powerful economy, little was done by the UPA government to build upon the strong foundation laid by the previous NDA government. In the years between 2004 and 2008, the economy grew fast, thanks to the lagged effects of the reforms of the NDA government and favorable global conditions. The UPA government took credit for the high growth but did little to consolidate it. The failure to take advantage of the years of high growth to strengthen the budget position of the government and invest in infrastructure to boost future growth prospects stood exposed. Worse, the UPA government, in its quest to maintain high economic growth by any means after the global financial crisis of 2008, severely undermined the macroeconomic foundations. The below are the inflation numbers during UPA govt:

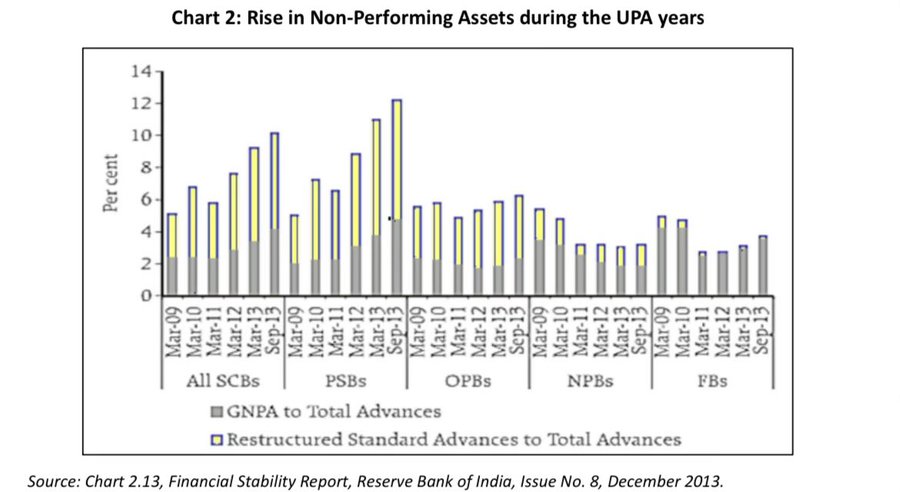

The banking crisis was one of the most important and infamous legacies of the UPA government. When the Vajpayee-led NDA government took office, the Gross Non-Performing Assets (GNPA) ratio in Public Sector banks was 16.0 per cent, and when they left office, it was 7.8 per cent. In September 2013, this ratio, including restructured loans, had climbed to 12.3 per cent largely because of political interference by the UPA government in the commercial lending decisions of public sector banks (Chart 2). Worse, even that high percentage of bad debts was an underestimate.

The banking crisis in 2014 was massive, and the absolute sum at stake was too large. Gross advances by public sector banks were only `6.6 lakh crore in March 2004. In March 2012, it was `39.0 lakh crore. Further, not all problem loans were recognized. There was much under the hood. According to a Credit Suisse report published in March 2014, the top 200 companies with an interest coverage ratio of less than one owed about `8.6 lakh crore to banks. Nearly 44 per cent of those loans (`3.8 lakh crore) were yet to be recognized as problem assets. In an era where capital flows dominate, India’s external vulnerability shot up because of over-dependence on external commercial borrowings (ECB). During the UPA government’s tenure, ECB rose at a compounded annual growth rate (CAGR) of 21.1 per cent (FY04 to FY14), whereas in the nine years from FY14 to FY23, they have grown at an annual rate of 4.5 per cent. No surprise, therefore, that our economy was in a vulnerable position in 2013 when the US dollar rose sharply. The UPA government had compromised external and macroeconomic stability, and the currency plunged in 2013. From its high to low, against the US dollar between 2011 and 2013, the Indian rupee plunged 36 per cent. The famous Foreign Currency Non-Resident (FCNR(B)) deposit window for NRIs was actually a call for help when there was a large depletion of the foreign exchange reserves. Under the UPA government, foreign exchange reserves had declined from around USD 294 billion in July 2011 to around USD 256 billion in August 2013. By end-September 2013, forex reserves were just enough to finance little over 6 months of imports, down from 17 months in end-March 2004. Forex reserve to external debt ratio tanked from 95.8 per cent in FY11 to 68.8 per cent in FY14. To salvage an ever-worsening situation, the Reserve Bank of India (RBI) opened a special window for FCNR (B) to attract USD deposits at a high premium in August-September 2013.

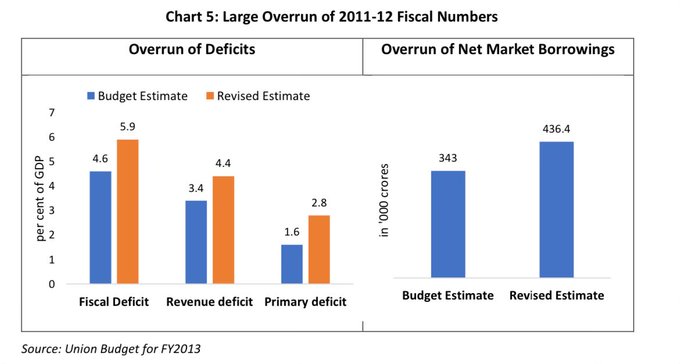

As a result of its fiscal mismanagement, the UPA government’s fiscal deficit ended up being far higher than it had expected, and it subsequently ended up borrowing 27 per cent more from the market than what it had budgeted for in 2011-12.

the pretext of responding to the impact of the global financial and economic crisis (while arguing, at the same time, that India was not affected by the crisis), the UPA government expanded its borrowing and did not relent at all. As per RBI, “the size of the government’s net market borrowing programmed (dated securities) increased nearly 9.7 times in eight years to ` 4.9 trillion in 2012-13. In addition, the government resorted to additional funding of ` 1.16 trillion through 364-day treasury bills.